Except you are new to opening bank cards, you are most likely accustomed to Chase’s 5/24 rule. Put merely, the rule is that this: if you happen to’ve opened 5 or extra private bank cards throughout all issuers within the final 24 months, Chase nearly actually will deny your subsequent card software.

Though some cobranded playing cards was once exempt from the rule, it now applies to nearly all Chase-issued playing cards — together with business cards (although they will not add to your private card rely if you have already got them and are making use of for a brand new private bank card).

To keep away from losing your five Chase slots or making use of for a Chase card solely to be denied, it’s best to preserve monitor of your 5/24 standing. Doing so may be very simple and would not require any difficult spreadsheets.

The quickest strategy to verify your 5/24 standing is through the use of Experian’s web site and cellular app.

Find out how to calculate your 5/24 standing

You may use virtually any free credit report monitoring service to calculate your standing. Whereas you are able to do this manually by tediously checking every account, let’s save these choices for later. First, let us take a look at the quickest possibility.

Kind by date with Experian

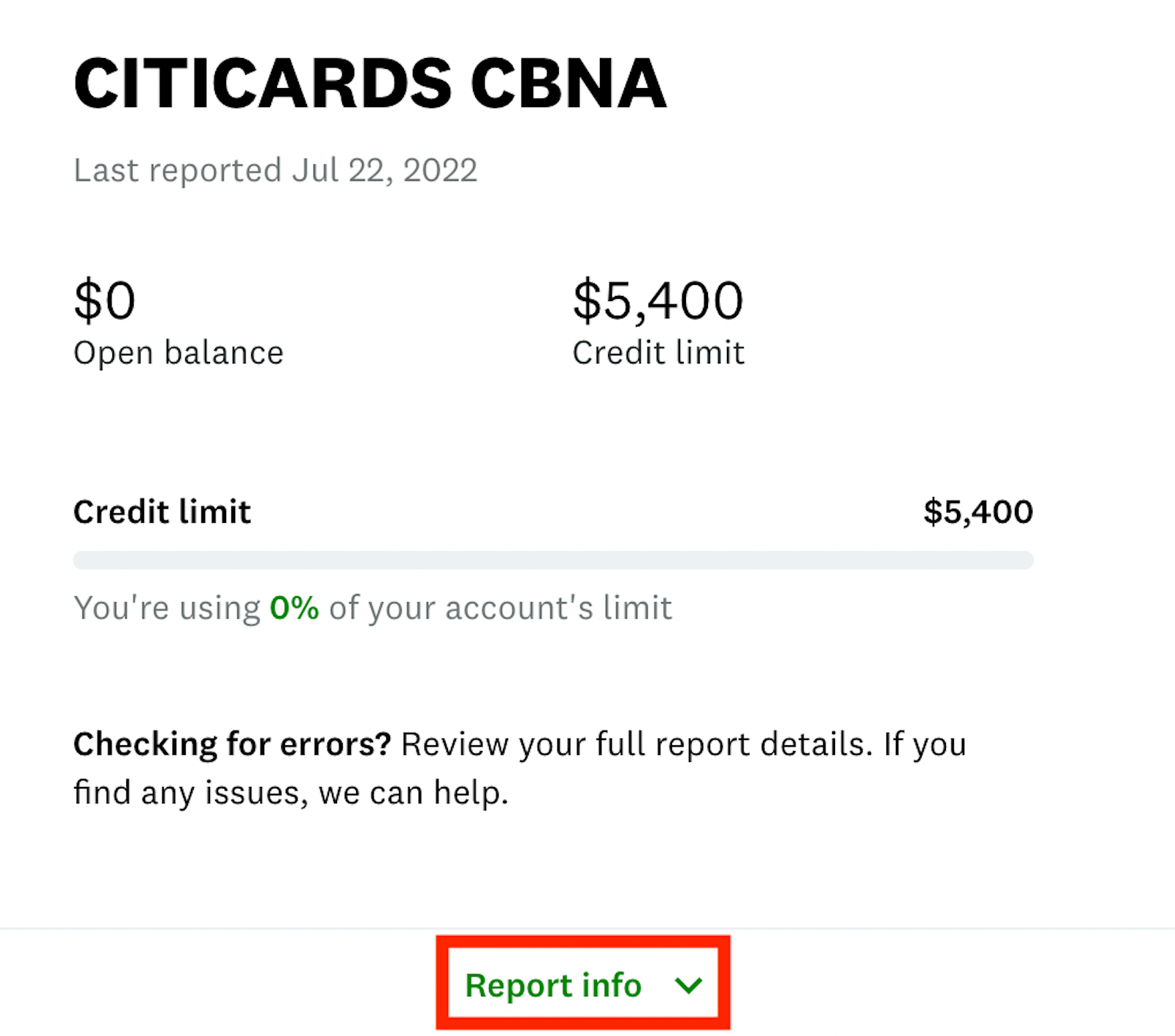

To begin, join a free account with Experian. Organising your account is simple. You may be requested for some private info and should confirm your id via safety questions.

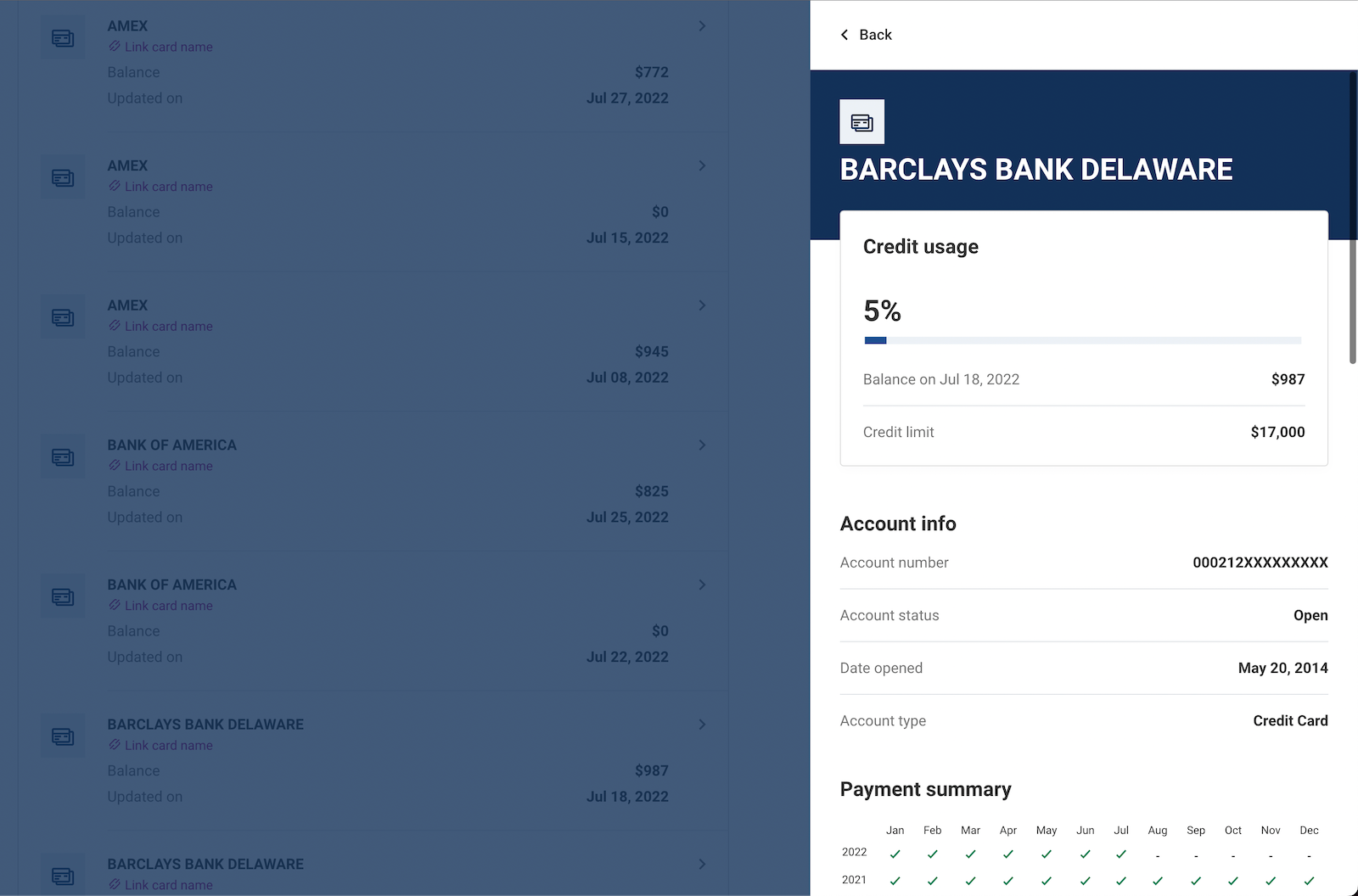

When you’re viewing your credit score report, you may view an inventory of all of your accounts — open and closed — sorted alphabetically by financial institution and bank card issuer on the desktop model of the web site.

Sadly, you could click on on every account individually to view the opening dates.

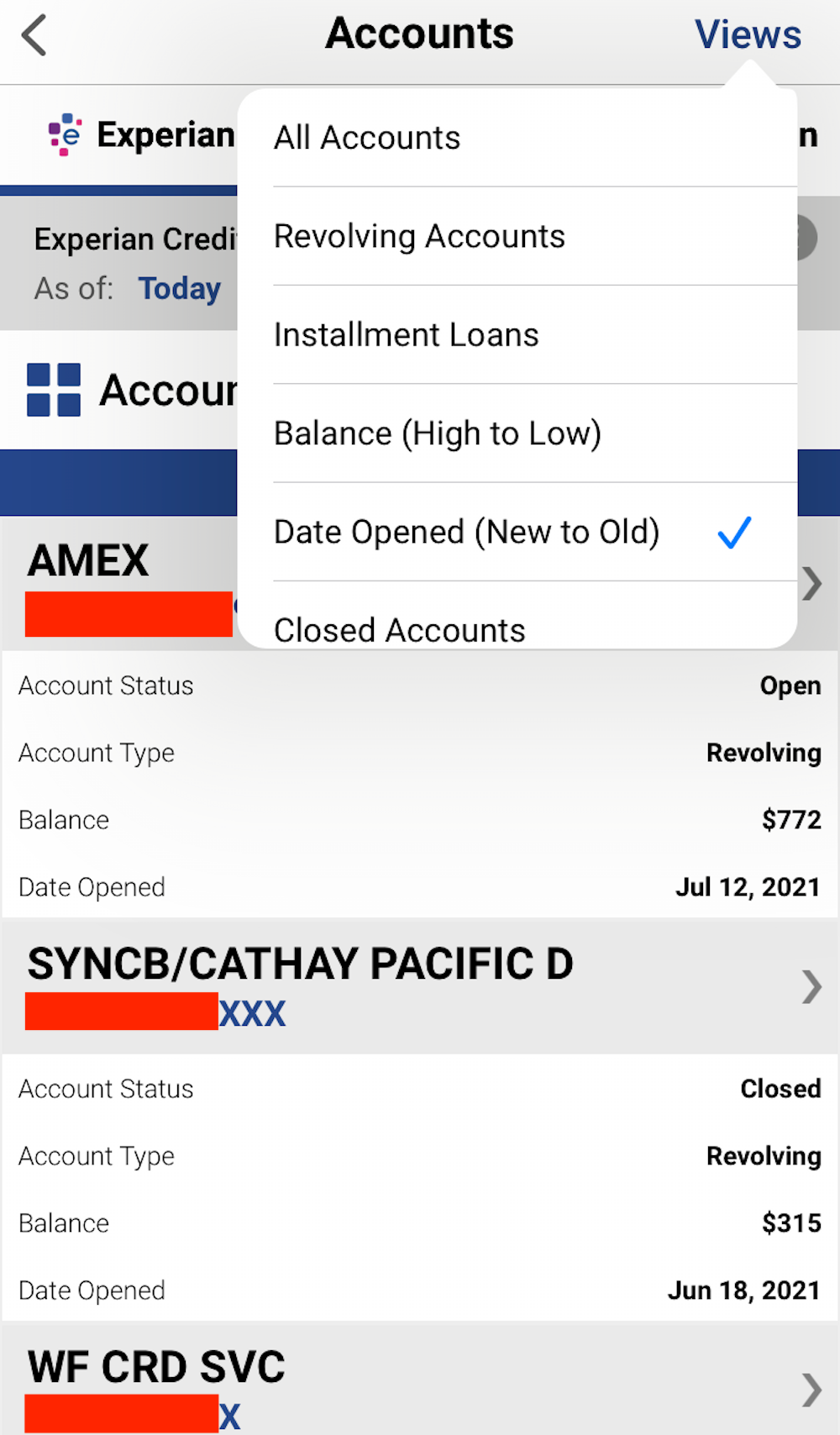

Nonetheless, the cellular app could make this a lot simpler. Inside the app, go to your credit score report, click on in your accounts, after which choose “Views” within the high proper nook. From right here, you may select “Date Opened (New to Outdated).”

Every day E-newsletter

Reward your inbox with the TPG Every day e-newsletter

Be part of over 700,000 readers for breaking information, in-depth guides and unique offers from TPG’s consultants

On this view, rely all the things that you just opened inside the previous 24 months.

It is essential to notice that Chase solely examines whether or not an account was opened. In case you’ve closed an account that was opened within the final 24 months, it nonetheless counts towards your standing. Additionally, information factors counsel that you’ll want to attend till the primary day of the twenty fifth month after your fifth account was opened to really be beneath the 5/24 restrict — that is an essential technicality.

Chase’s pc techniques will add authorized-user playing cards from one other particular person’s private credit score or cost card to your 5/24 rating, as they’re reported in your credit score report. Nonetheless, if you happen to’re in any other case underneath 5/24, you may nonetheless apply for a Chase card and name the reconsideration line to ask that these accounts not be thought of. Additionally, notice that auto loans, pupil loans and mortgages present up in your credit score report however don’t rely towards your 5/24 quantity.

Guide strategies for checking your 5/24 quantity

Your free credit score report from the three main companies would not can help you kind your accounts by the date they have been opened. Nonetheless, you may nonetheless set up your 5/24 standing by acquiring a free credit score report or by clicking on every account on Experian’s desktop browser or different comparable credit score report trackers.

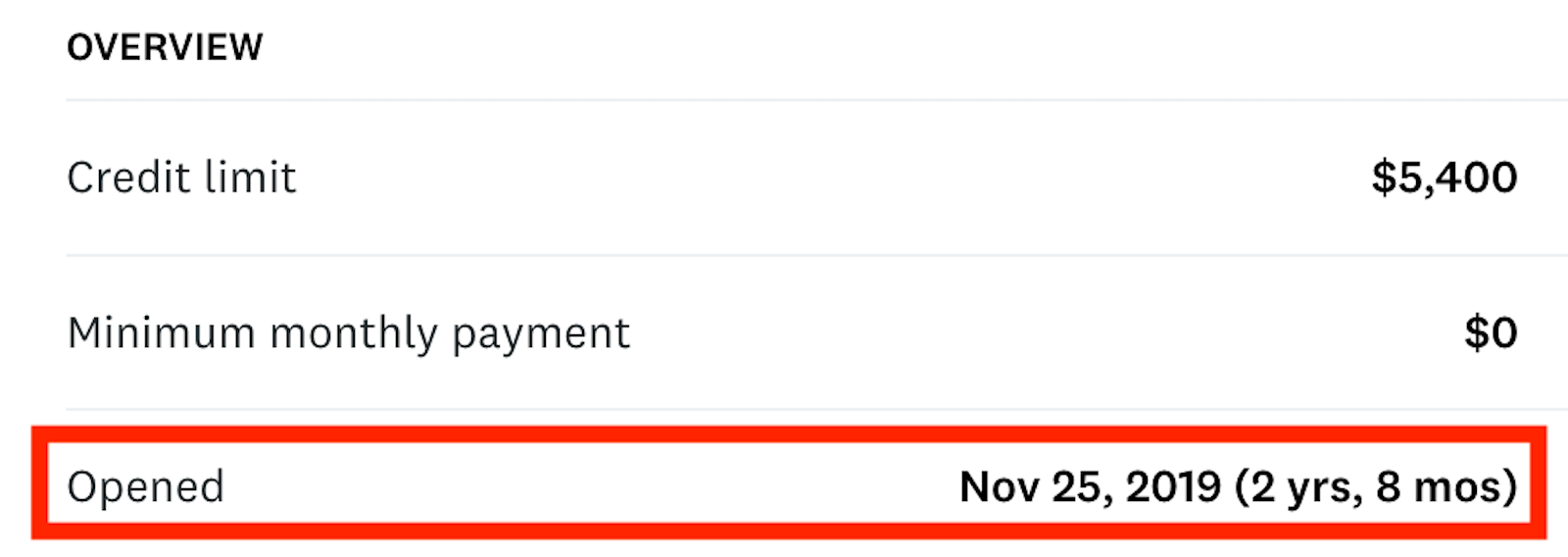

From right here, you may see your account opening date.

What to do if you happen to’re underneath 5/24

Your first plan of motion needs to be to use for the Chase trifecta, which consists of the Chase Sapphire Reserve®, Chase Freedom Unlimited® (or Chase Freedom Flex®) and Ink Business Preferred® Credit Card. Utilizing these playing cards collectively will can help you maximize the Ultimate Rewards program and provide help to benefit from your on a regular basis purchases.

Nonetheless, the cardboard alternatives do not finish there. There are a number of different Ultimate Rewards points-earning cards, in addition to loads of profitable cobranded airline and resort playing cards price contemplating, such because the United℠ Explorer Card and the World of Hyatt Credit Card.

Associated: The best ways to use your Chase 5/24 slots

What to do if you happen to’re over 5/24

Some factors lovers swear by Chase and refuse to use for different playing cards after they’re over 5/24. That might be a giant mistake. The “opportunity cost” of ready a number of months to use for one more bank card — within the hopes of selecting up a single Chase card, although approval shouldn’t be assured — is way too excessive. Plus, it is at all times a good suggestion to diversify your incomes technique.

Your choices for beneficial playing cards outdoors of the Chase ecosystem are countless. As an illustration, American Express has its own trifecta of cards that may unlock a strong mixture of incomes charges, welcome presents and perks — The Platinum Card® from American Express, the American Express® Gold Card and The Blue Business® Plus Credit Card from American Express. Then there are all of Amex’s cobranded playing cards, such because the Marriott Bonvoy Brilliant® American Express® Card and the Delta SkyMiles® Platinum American Express Card.

And that is earlier than you even take into account all the different issuers on the market, comparable to Bank of America, Capital One and Citi.

Associated: The best cards to get after you hit 5/24

Backside line

To maximise Chase’s bank card lineup, you should be smart about which playing cards you get and while you apply for them. Calculating your 5/24 standing is simple due to free credit score report monitoring companies like Experian. In case you’re over 5/24, do not make the error of overlooking playing cards from different issuers.

For extra on Chase’s 5/24 rule, see these associated articles:

Trending Merchandise